This analysis was originally posted by Audit Analytics.

Audit Analytics recently released a new report, Monitoring the Audit Market in Europe. Using our extensive databases, our analysts compiled this timely report which examines the impacts of the European Commission’s 2014 Audit Directive and Audit Regulation. These two pieces of legislation were adopted in response to concerns identified in the audit process following the financial crisis of the late 2000s and early 2010s.

The legislation sought to fundamentally revamp the audit profession to increase audit quality. In our report, we examine the impacts these two pieces of legislation have had on the audit market in the European Union.

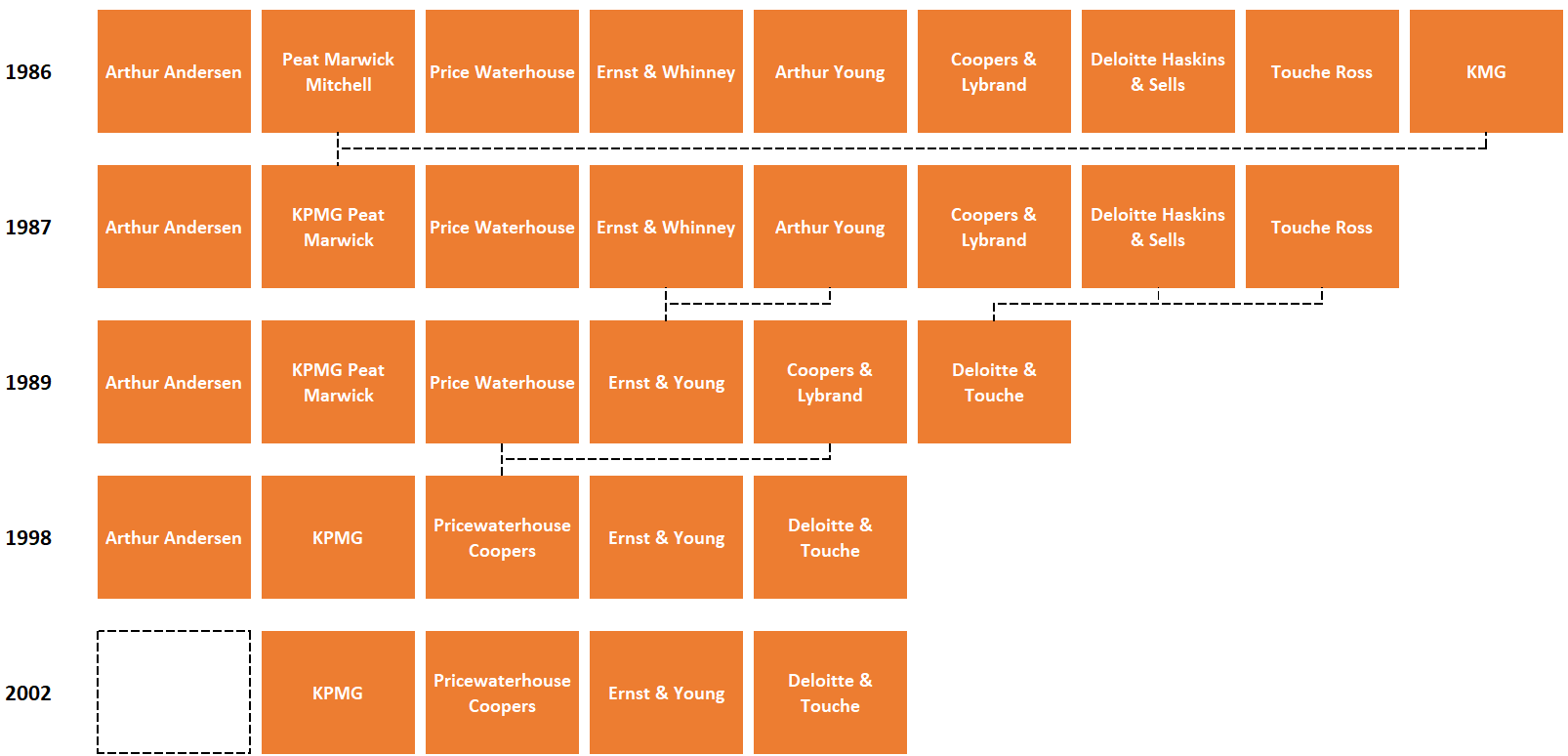

The report begins by reviewing the current state of the audit market. Nearly three decades after the collapse of Arthur Andersen, the audit market has never fully recovered. The major issue for the audit market does not appear to be lack of competition; the four largest firms appear to compete quite fiercely. Rather, the fear is what would happen if one of the remaining four were to fall.

As Arthur Andersen proved, it is not impossible for a large firm to exit the market. One problem for audit firms in many European Union member states is that there are no liability caps. For example, BDO Spain was recently ordered to pay part of a €126.8 million settlement following the collapse of Pescanova. BDO earned just €2 million between 2011 and 2013 for the audits it performed for Pescanova.

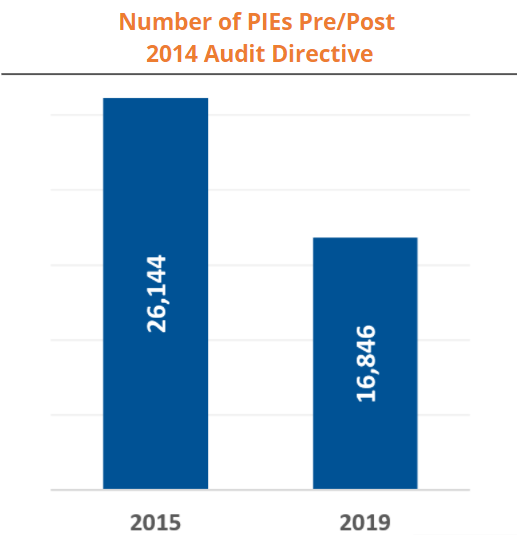

Next, the report reviews differences in the member state markets and trends in the number of public interest entities (PIEs) and listed entities – those PIEs that have equity securities listed on a regulated exchange. The 2014 Audit Directive amends the previous definition of a public interest entity, but still provided only a minimum definition; member states are free to expand the definition however they see fit.

The new definitions significantly reduced the number of PIEs. This was not due to the Audit Directive definition, rather, to individual member states. Most significantly, Spain’s narrower definition slashed the number of PIEs by 80%. Many believe the narrower definitions are a sign that member states believed the new rules and regulations established by the legislation were overly severe.

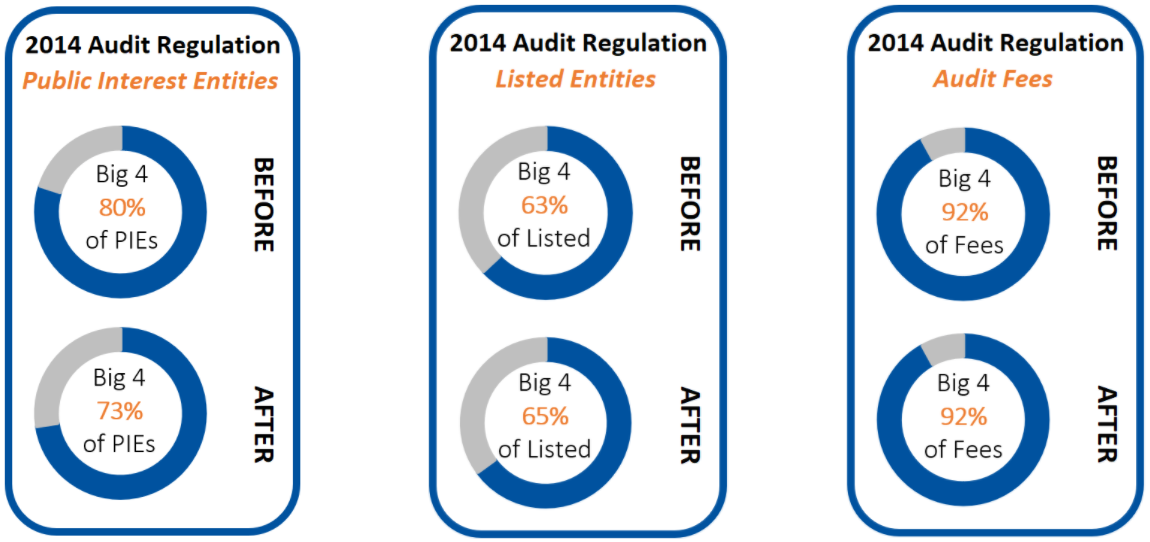

The report then indirectly examines competition through the lens of market concentration. One of the major goals of the legislation was to create an audit market with more participants, with the idea that more participants would lead to more competition, and, in turn, more competition would incentivize higher quality audits.

When looking at the PIE market, we see that the percentage of the market audited by Big 4 firms has dropped considerably. However, as mentioned above, the definitional change of PIEs in some member states has made the evaluation less comparable.

Instead, looking at the listed entities market, we see that the Big 4 have a large percentage of clients since the implementation of the new rules and regulations. Additionally, there has been no impact on the audit fees earned by the Big 4 relative to total audit fees.

Lastly, the report reviews independence. A key component of the European legislation was to ensure greater independence between audit firms and their clients. This idea has persisted post implementation with the UK announcing operational separation or Big 4 firms early this year.

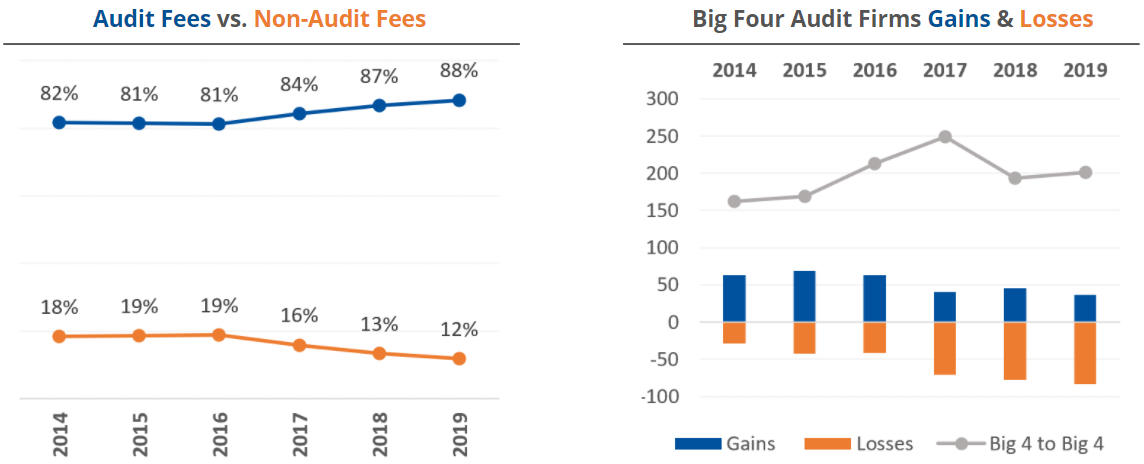

The legislation imposed limitations and bans on non- audit services, as well as maximum tenures to enhance auditor independence; non- audit services were capped at 70% of the average of audit fees incurred by the PIE in the previous three years; many tax, valuation, and consulting services were banned; and tenures were capped at 20 years for single audits and 24 years for an audit with more than one audit firm.

As shown above, the legislation was effective at reducing the amount of non-audit services provided by audit firms. Overall, the amount of non- audit fees earned by audit firms fell from nearly 20% of total fees to just over 10%.

Similarly, the limitations on tenure have appeared to work at creating a more diverse audit market. Prior to the legislation, more companies were engaging Big 4 audit firms after leaving smaller audit firms (as shown in blue). Post legislation, more companies are engaging smaller audit firms after leaving a Big 4 firm (as shown in orange). Though, most companies continue to switch from one Big 4 firm to another Big 4 firm (as shown in grey).

It is still early for the legislation. While it is important to observe the impacts the legislation is having on the market, it is also important to understand that fundamental change takes time. As we can see, particularly with non- audit fees and auditor changes, the audit market is continuing to adjust in response to the legislation.

For a copy of the full report, please click here.

For more information about Audit Analytics or this analysis, please contact us.

Interested in our content? Be sure to subscribe to receive our email notifications.