This analysis was originally posted by Audit Analytics.

The audit opinion is particularly important to stakeholders, as it provides insight into whether the financial statements are true and reliable for decision making. When an opinion is issued, auditors generally include an explanation for their decision. Because most opinions are unqualified (clean) and issued when an auditor determines that the financial records are appropriate and maintained in accordance with regulations, it is important for stakeholders to take note when modified opinions are issued.

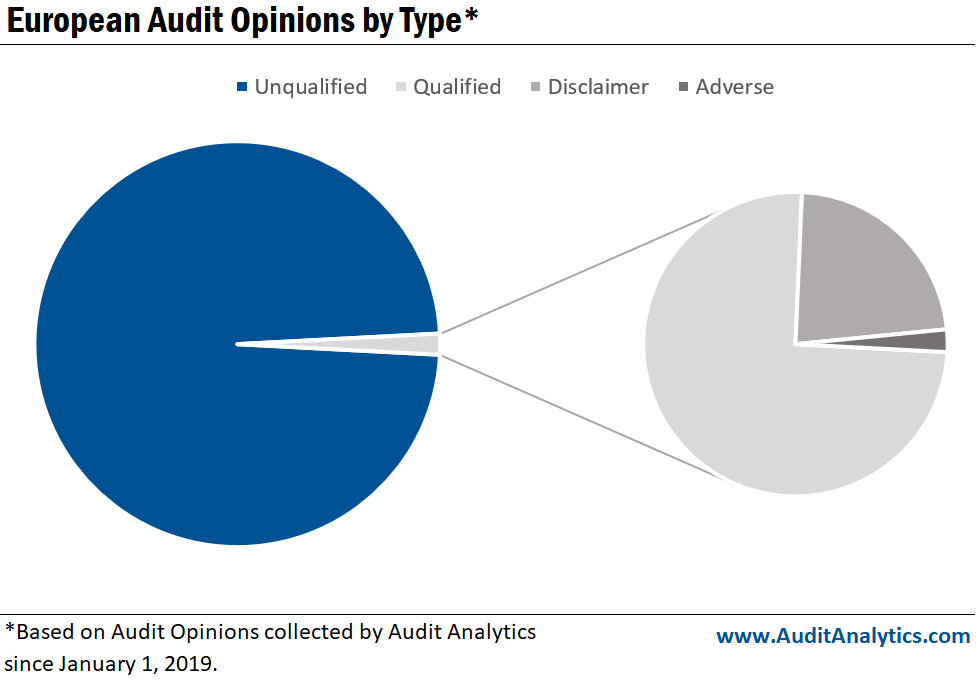

Modified opinions are classified by the severity of misstatements, pervasiveness, and sufficiency of the audit evidence obtained in accordance with ISA 705. The types of modified opinions collected include qualified, adverse, and disclaimer of opinion. The chart below shows the percentage of opinion types recorded by Audit Analytics since the beginning of 2019.

What makes an unqualified opinion – that judges financial statements to be presented fairly and appropriately – different from a modified opinion?

Qualified Opinions

A qualified opinion is a modified opinion in which an auditor has found material misstatements in the financial statements, but they are not pervasive. Usually, the misstatement is a single issue.

Take, for example, the 2019 opinion issued to Hochdorf Holding (SIX:HOCN) by Ernst & Young on the annual financial statements. In conjunction with the qualified opinion, EY also included a going concern modification, citing that the repayment of loans to the Company is crucial for “the achievement of budget targets,” and that the uncertainty of receiving these payments creates uncertainty for Hochdorf Holding to continue as a going concern. EY then states that, other than this issue, “the consolidated financial statements for the year ended 31 December 2019 give a true and fair view of the financial position…”

Disclaimer of Opinion

Another type of modified opinion we record is a disclaimer of opinion. This type of opinion is not actually an opinion, but rather the auditor stating that they were unable to obtain sufficient and appropriate audit evidence to issue an opinion. This can happen for several reasons including:

• The auditor was unable to obtain necessary financial records and/or unable to complete all audit procedures;

• Financial statements were withheld from the auditor due to a lack of trust on auditor independence; or

• Lack of communication and clarification leading to misunderstanding or lack of supporting financial documents.

In September, a disclaimer of opinion was issued by Grant Thornton to Mothercare PLC (LON:MTC), a company specializing in maternity and children’s clothing, for its FYE 28 March 2020 financial statements. Grant Thornton cited several reasons for issuing the disclaimer, including the uncertainty of the company’s ability to continue as a going concern, a lack of supporting information regarding the company’s retail operations, and limited availability of audit evidence concerning inventory. Unsurprisingly, as seen in other large companies in a previous blog, COVID-19 appears to be at the core of this company’s difficulties.

Adverse Opinion

The rarest type of opinion is an adverse opinion. This type of opinion is issued when the financial statements contain significant material misstatements that are pervasive – meaning the misstatements impact multiple sections of the financial statements.

BDO clearly states why an adverse opinion was issued in the 2019 annual financial statements for the LumX Group, which delisted from the Swiss Exchange in June 2020.

“We are of the opinion that the risks linked to the recoverable amount of the goodwill are not sufficiently reflected in the impairment considerations applied by the Group, and are of the opinion that the carrying value of the goodwill is overstated by USD 21.1 mios resulting in an understatement of the Loss of the year and an overstatement of the Total equity in the same amount. As a consequence, the relevant impairment disclosures are missing in Note 12. In our opinion, this has a pervasive and material impact on the financial statements.”

This opinion made headlines in the Financial Times where they flush out the “damning report on the group’s financial statements.”

The difference in the modified opinion issued by EY for Hochdorf and BDO’s modified opinion for LumX is that EY qualified the Hochdorf opinion due to a single issue caused by the uncertain payment of the receivables, whereas BDO issued an adverse opinion due to the pervasive misstatements found in LumX’s financial misstatements.

Reasons such as these highlight the importance of not only the audit opinion, but the type of audit opinion issued to a company. Tracking these modified opinions has never been easier with the help of Audit Analytics.

This analysis uses data from the Europe Audit Opinions database, powered by Audit Analytics.

For more information about Audit Analytics or this analysis, please contact us.

Interested in our content? Be sure to subscribe to receive our email notifications.