This analysis was originally posted by Audit Analytics.com

Earlier this week, the Financial Conduct Authority (FCA) and the Financial Reporting Council (FRC) reminded companies in the UK that the permission to delay publication of financial reports is still in effect. The initial joint statement was issued in the early days of the lockdown in the UK on 26 March 2020.

The relief, prompted by the challenges of publishing accurate financial information in the midst of the pandemic, allows listed companies on regulated markets to delay publishing their annual financial reports for two months, and their half-yearly reports for one month.

In an earlier letter to CEOs, CFOs, and Audit Committee Chairs dated 12 November 2020, the FRC stated,

“we encourage companies to consider carefully whether they should lengthen their reporting timetables for 2021, making use of the extensions to reporting deadlines announced by the FCA, which remain in place.”

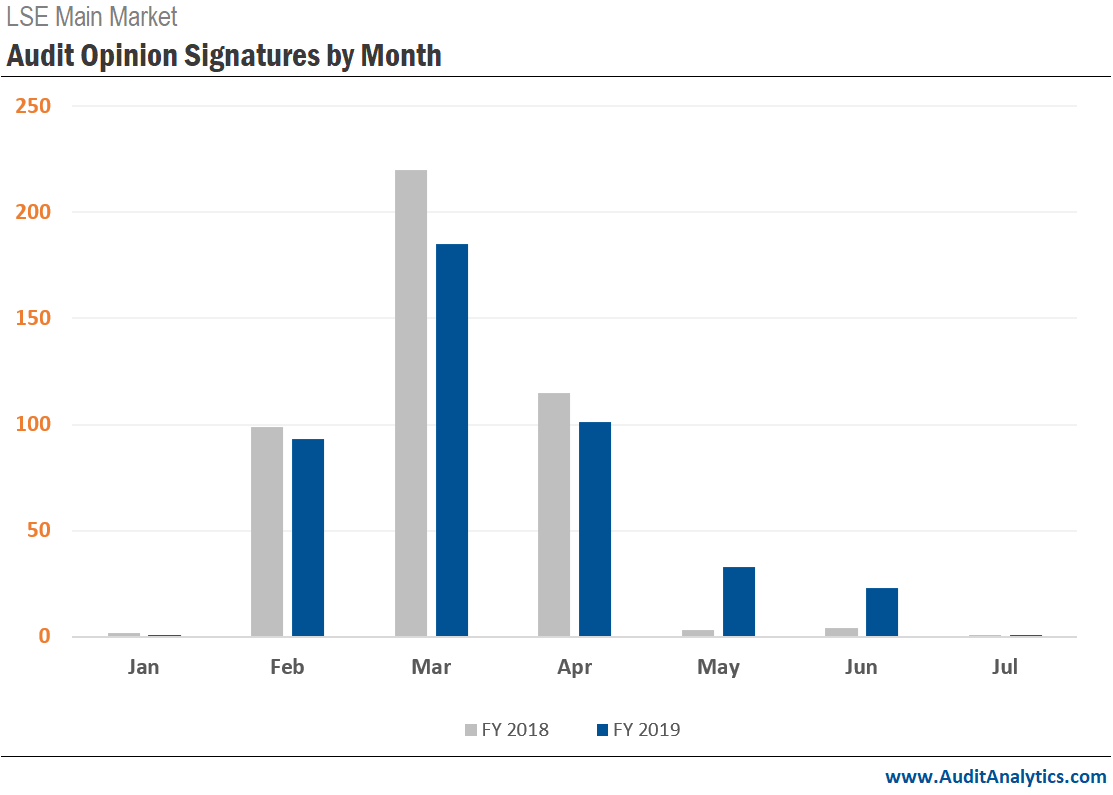

Audit Analytics noted that for fiscal year 2019, 13% of companies with December year- ends had their opinions signed between May and July 2020 (after the four-month deadline), a significant difference compared to just 2% for fiscal year 2018 opinions signed in 2019.

Amid the COVID-19 backdrop, accurate corporate reporting is more important than ever; however, obtaining critical information is more challenging than it has ever been in the memories of financial teams, audit firms, and executives. To further complicate the issue, UK companies continue to face the uncertainties brought about by Brexit.

The FRC reminded companies of the need for transparency to investors regarding:

In December 2020, the FRC addressed the challenges of accurate going concern disclosures for companies in their report, Going Concern, Risk, and Viability. Citing a number of examples and scenarios, the FRC provided a framework for how companies can best assess and report on the uncertain future their firms are facing.

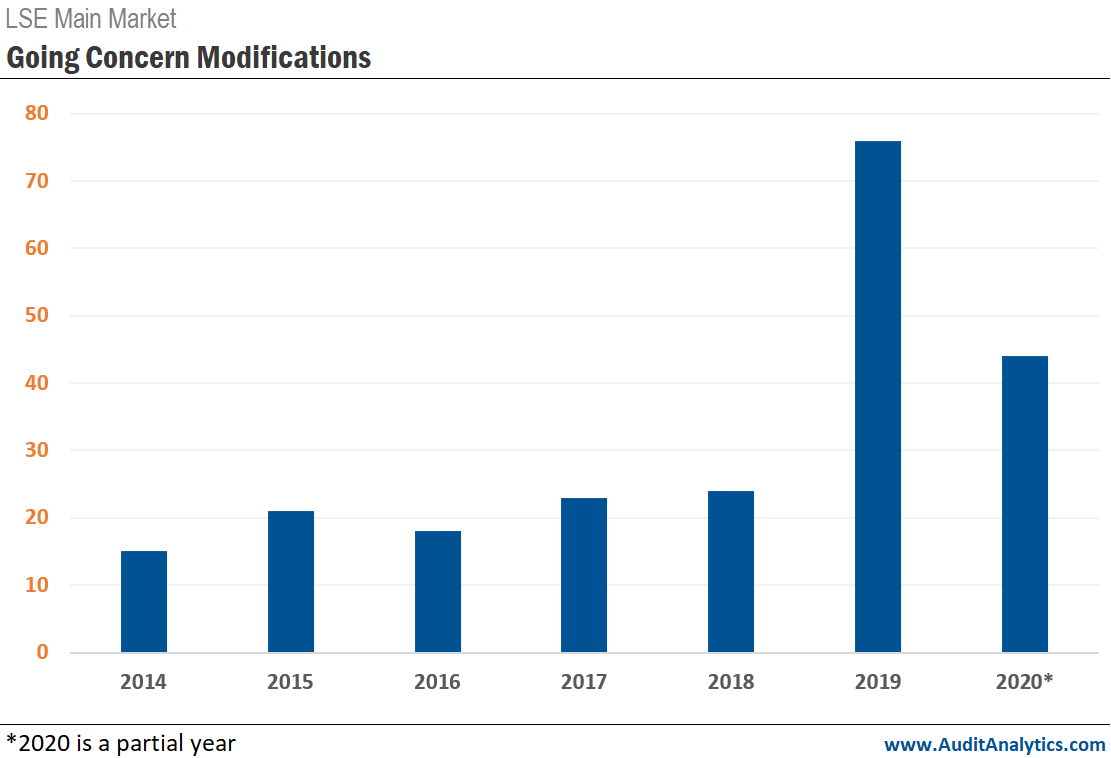

On the LSE Main Market, Audit Analytics recorded 76 audit opinions with going concern modifications in fiscal year 2019. The number disclosed to date for fiscal year 2020 is almost double the number from 2018. We expect this number to go up significantly when the 31 December 2020 fiscal year end reports begin to trickle in during the coming weeks and months.

This analysis uses data from the Europe Audit Opinions database, powered by Audit Analytics.

For more information about Audit Analytics or this analysis, please contact us.

Interested in our content? Be sure to subscribe to receive our email notifications.