This analysis was originally posted by Audit Analytics.

Note: This analysis will be updated to reflect 2020’s market share once all annual reports have been filed.

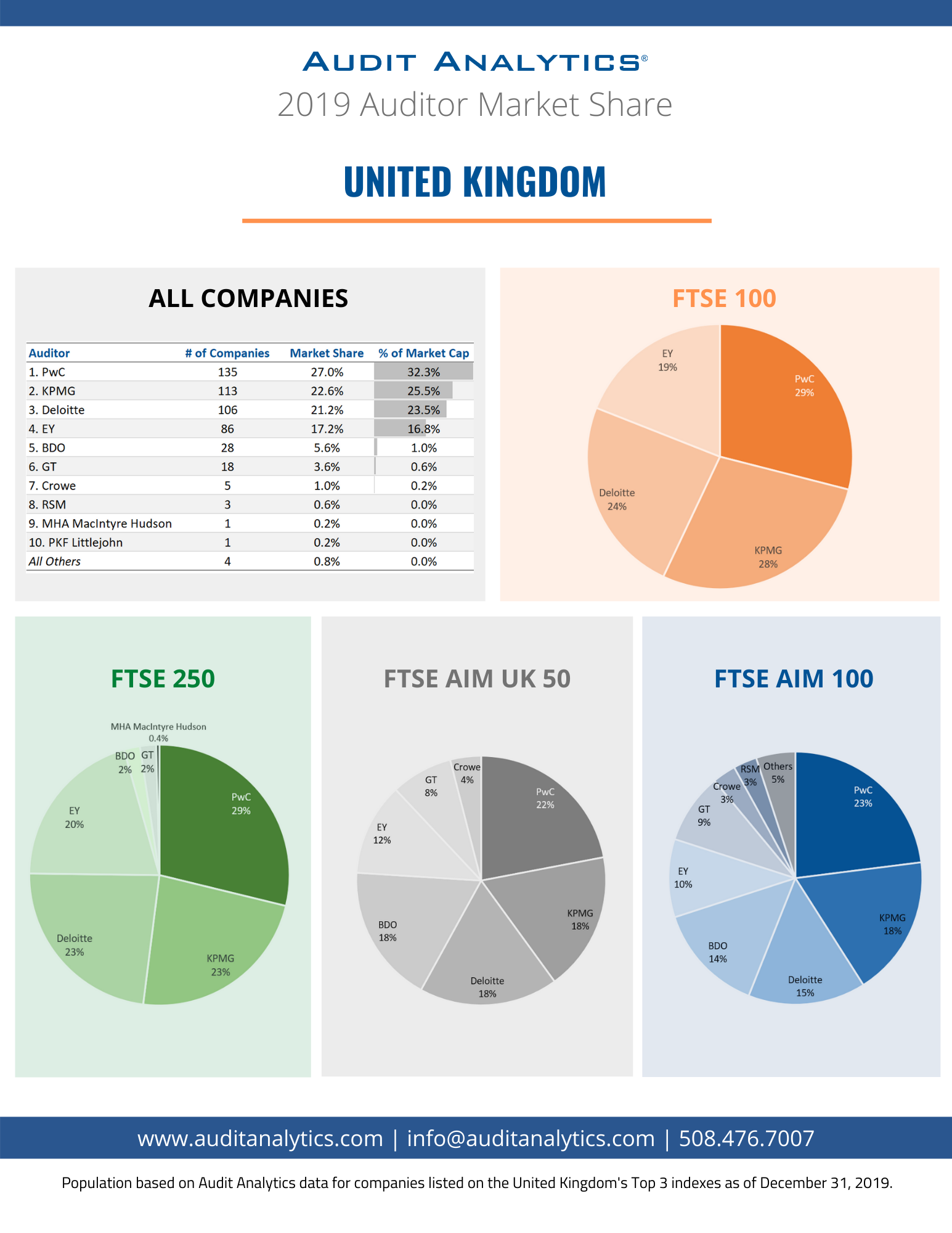

Audit market share was highly concentrated among the top indexes in the United Kingdom at the end of 2019. PwC captured the highest percentage of the market, auditing 27% of London Stock Exchange index-listed companies. The rest of the Big Four combined audited 61% of the remaining companies. BDO and Grant Thornton chimed in with 6% and 4%, respectively. Eight firms audited the remaining 3% of companies.

In this post, we examine four London Stock Exchange indexes: FTSE 100, FTSE 250, FTSE AIM UK 50, and FTSE AIM 100.

In 2019, FTSE 100, the top London index with a combined market cap of £1.8 trillion, was audited exclusively by the Big Four. Like all the large cap indexes examined in this analysis, PwC took the top spot (29%), followed by KPMG (28%), Deloitte (24%), and EY (19%).

In 2020 and 2021, we have recorded a number of auditor changes, as well as noted new constituents on the FTSE 100. The net effect of these changes will knock PwC from the top spot to share last place with Deloitte. KPMG, despite the negative publicity brought about by the failure of Carillion, will take the lead, auditing 29 of the FTSE 100 companies. EY, still reeling from the recent Wirecard scandal, will audit 25 companies.

The FTSE 250 is comprised of the top companies by market cap after the FTSE 100, with a total market cap of £394.6 billion. The Big Four ranked the same in the FTSE 250 as in the 100 in 2019. However, in the FTSE 250 we saw a few challenger firms in the mix. BDO and Grant Thornton each audited five companies and MHA MacIntyre Hudson audited one, giving non-Big Four firms 4% of the market share.

During 2020 challenger firms’ market share experienced significant growth. Non-Big Four firms now account for 9% of the market. BDO takes most of the credit with 15 engagements of FTSE 250 companies. They are followed by Grant Thornton with four, MHA with two, and RSM with one. It is possible that these changes are due in part to the efforts of UK regulators to loosen the Big Four’s hold on the market.

The FTSE AIM UK 50 consists of the companies with the highest market cap on London’s unregulated market, AIM. At the end of 2019, PwC took the top spot, auditing 11 companies. BDO, KPMG, and Deloitte each audited nine companies. EY came in fifth with six clients. Grant Thornton and Crowe audited four and two companies, respectively. Collectively, the three non-Big Four firms held 30% of the FTSE AIM UK 50 market share in 2019.

Since 2019, auditor changes and changes in the index composition have resulted in PwC expanding their reach to 13 companies. BDO continues to audit nine, followed by Deloitte auditing eight, EY with seven, KPMG with six, and Grant Thornton auditing four. Crowe, Jeffreys Henry, and RSM are each engaged by one company in the FTSE AIM UK 50.

The FTSE AIM 100 contains all companies on the UK 50 plus the next 50 companies listed on AIM by market cap. In 2019, 13 firms audited this index; again, PwC audited the most companies. The next four firms, as with the UK 50, were KPMG, Deloitte, BDO, and EY. In addition to the auditors of the UK 50, Kreston Reeves, Mazars, PKF Littlejohn, and MNP each audited one company.

Since 2019, Audit Analytics has noted some shifting in the FTSE AIM 100 market share. Most notably, EY lost seven of its ten clients and is now engaged by just three. Also noteworthy, PKF Littlejohn picked up three additional clients and Mazars gained one.

The reduction in the concentration of the FTSE 250, AIM UK 50, and AIM 100 are positive signs in a market that is aiming to reduce the risk of a single point of failure like the one that occurred when Arthur Andersen collapsed in 2002. Time will tell whether a challenger firm will be able to break into the tightly held FTSE 100 in the coming years.

Since EU Audit Reform in 2014, the United Kingdom has followed the regulations implemented by the European Parliament, taking advantage of the permission to alter the key audit partner rotation from seven to five years and permitting only minimal tax and valuation services. Post-Brexit, the Department for Business, Energy, and Industrial Strategy (BEIS) has implemented new UK Audit Regulations. These mainly relate to third country rights, meaning who can audit European Economic Area companies listed in the UK. The regulations do not affect group audits for EEA companies with subsidiaries in the UK.

This analysis uses data from the Europe Audit Opinions and Auditor Changes databases, powered by Audit Analytics.

For more information about Audit Analytics or this analysis, please contact us.

Interested in our content? Be sure to subscribe to receive our email notifications.