This analysis was originally published by Audit Analytics.

Note: This analysis will be updated to reflect 2020’s market share once all annual reports have been filed.

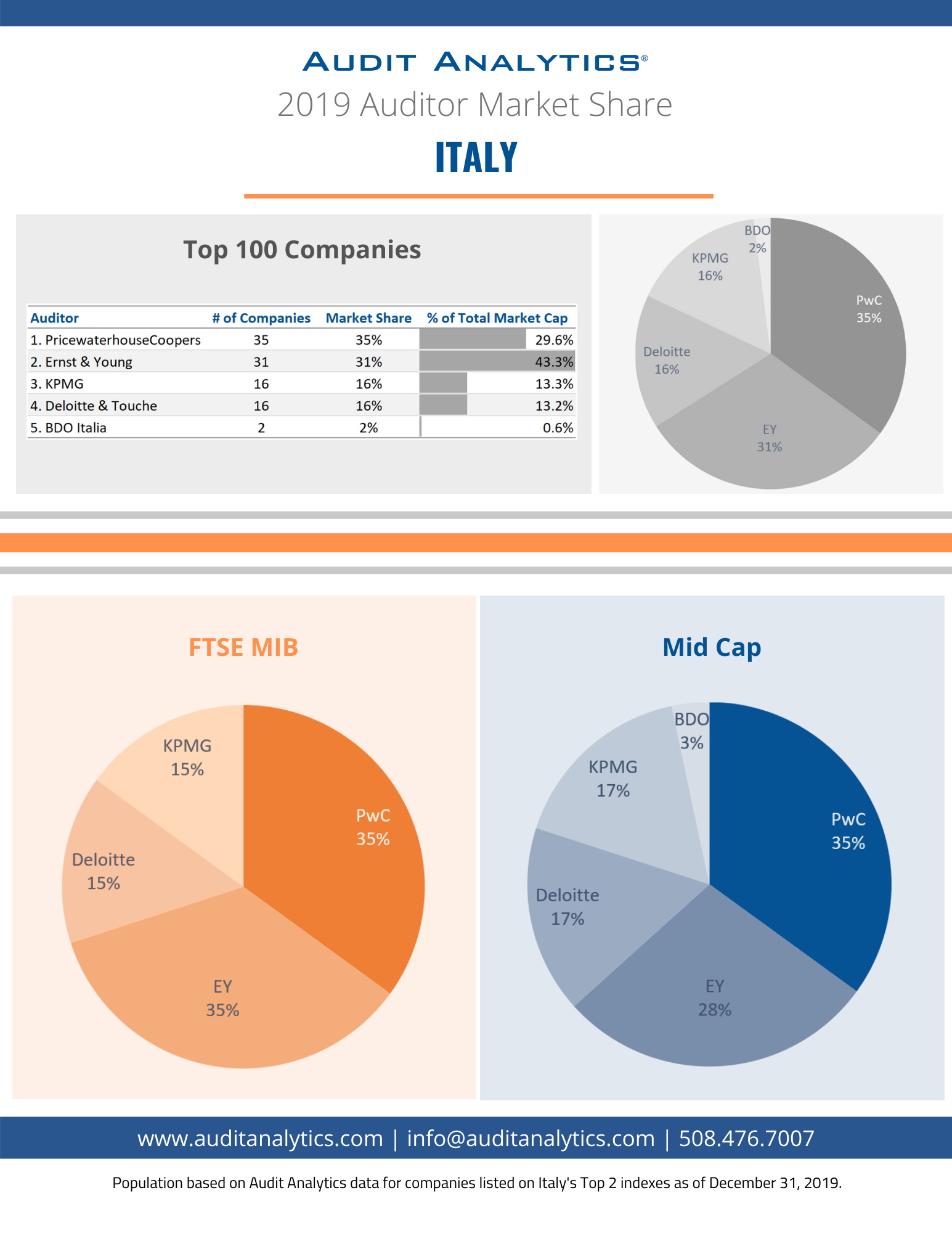

The Big Four firms account for a staggering 98% of the market share across Italy’s top 100 companies. Capturing the other 2% of the market is BDO, with just 2 companies; both of which are listed on the FTSE Italia Mid Cap. Interestingly, PwC has the largest number of clients and roughly 30% of the total market cap, while EY has 3 fewer clients, but roughly 13% more of the total market cap.

In total, there are five accounting firms that audit the top 100 companies listed on the Borsa Italiana. Here, we look at the auditor market share among Italy’s top two indexes: the FTSE MIB and the FTSE Italia Mid Cap.

FTSE MIB

This is the benchmark index, consisting of the top 40 companies trading on the Borsa Italiana. PwC and EY hold the lead here, each with 35% of the market share. Deloitte and KPMG each account for 15%, auditing less than half the companies of PwC and EY.

As noted in a previous blog, the FTSE MIB had five auditor changes in 2019. Deloitte was the only firm unaffected, though EY broke even by losing and gaining two companies. Meanwhile, PwC lost two clients and KMPG gained two, so we should expect to see a small shift in the 2020 market share.

This index is composed of the next 60 largest companies. Here, we see a slight deviation from the market share of the FTSE MIB with the inclusion of BDO. Again, PwC holds 35% of the market share, though EY drops to 28%. Deloitte and KPMG tie again, each with 17%, while BDO joins the Big Four in this index, holding a share of 3%.

In 2019, there were six auditor changes among these 60 companies. The only firm to come out ahead was Deloitte, who gained two companies. EY and KPMG each lost one, PwC broke even, and BDO was unaffected.

Though Italy formally adopted the EU Audit Reform Directive 2014 policy in 2016, it was nothing new to the country, which first introduced mandatory auditor rotation in 1975. Since 1975, Italian law has required that public companies rotate audit firms after nine years and individual statutory auditors after seven years, making the rotation date relatively predictable.

In addition to adopting the EU Reform, Italy extended its definition of public interest entities (PIEs) beyond the EU scope. Included in Italy’s definition are pension funds, UCITS/ investment companies, asset management companies, electronic money institutions, and those that meet a size criterion.

This analysis uses data from the Europe Audit Opinions and Auditor Changes databases, powered by Audit Analytics.

For more information about Audit Analytics or this analysis, please contact us.

Interested in our content? Be sure to subscribe to receive our email notifications.