Can Management Control Impact Sustainable Behavior?

From prior research, we know that management control can impact employee motivation and behavior. In our new study, recently published in Public Administration Review, we find that sustainability-related management controls can stimulate pro-environmental behavior of employees. Below, we highlight our main findings.

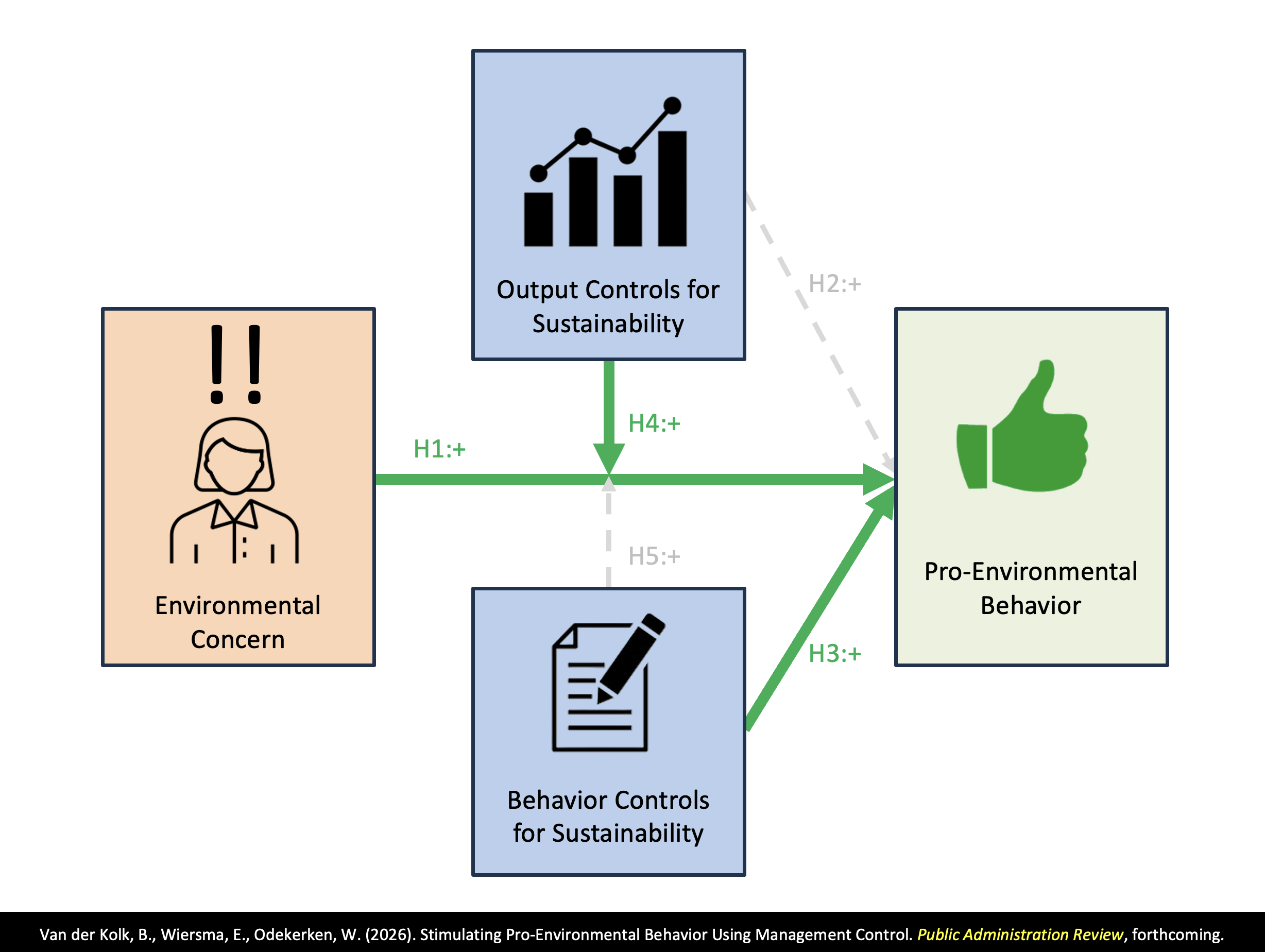

Pro-environmental behavior and management control

While CO2 levels are reaching record high levels, the scientific consensus is that it is “unequivocal that human influence has warmed the atmosphere, ocean and land” (IPCC 2023). We are interested in studying how the impact of human beings and organizations on climate can be prevented or mitigated, which is why we examine pro-environmental behavior in organizations.

Survey evidence was collected in a Dutch city government that is at the forefront of implementing sustainability-related forms of management control. We categorized their management control efforts in output control (e.g., a sustainability budget and a coalition agreement on sustainability goals), behavior control (e.g., a sustainability roadmap and compulsory sustainability formats for new proposals), and clan control (e.g., statements from senior management, training, and inspiration sessions).

Finding 1: Climate-concerned employees engage in more sustainable behavior

First, we find that employees who are more concerned about the climate, also engage more in pro-environmental behavior in the workplace (H1). This is in line with the theory of planned behavior, which states that actual behavior often correlates with intentions.

Finding 2: Output controls strengthen the relation between concern and behavior

Second, our findings suggest that the familiarity of employees with sustainability-related output controls strengthens the relation between employee concerns about the climate and their pro-environmental behavior (H4). We theorize this by arguing that budgets can signal a norm, and stronger social norms can strengthen the likelihood that employees translate their environmental concerns into action.

Finding 3: Behavior controls directly increase sustainable behavior

Third, our survey evidence suggests that behavior controls, such as formats that force employees to write about the climate impact of their proposals, directly impact pro-environmental behavior (H3). This finding is independent from the level of employee concerns about the climate. In other words, if employees have lower levels of concern for the environment, behavior controls can still be effective to increase their pro-environmental behavior.

Conclusion

Research in the field of management control and sustainability is still in development. We contribute to this literature by unpacking how different types of management control can help facilitate pro-environmental behavior. Have a look at our paper (open access) in Public Administration Review for more information about this study, its limitations, and its implications.

Full paper (open access)

Van der Kolk, B., Wiersma, E., Odekerken, W. (2026). Stimulating Pro-Environmental Behavior Using Management Control. Public Administration Review, forthcoming. https://doi.org/10.1111/puar.70156

Biographies

Berend van der Kolk is an Associate Professor of Management Accounting at VU Amsterdam.

Eelke Wiersma is an Associate Professor of Management Accounting at VU Amsterdam.

Willemijn Odekerken is a Senior Controller at a Dutch City Government.