This analysis was originally posted by Audit Analytics.

We will finish our review of accounting quality by looking at financial restatements in the UK. Over the past few years, the number of companies listed on the London Stock Exchange that have restated their financials has grown. This analysis includes companies listed on both the Main Market and the AIM Market.

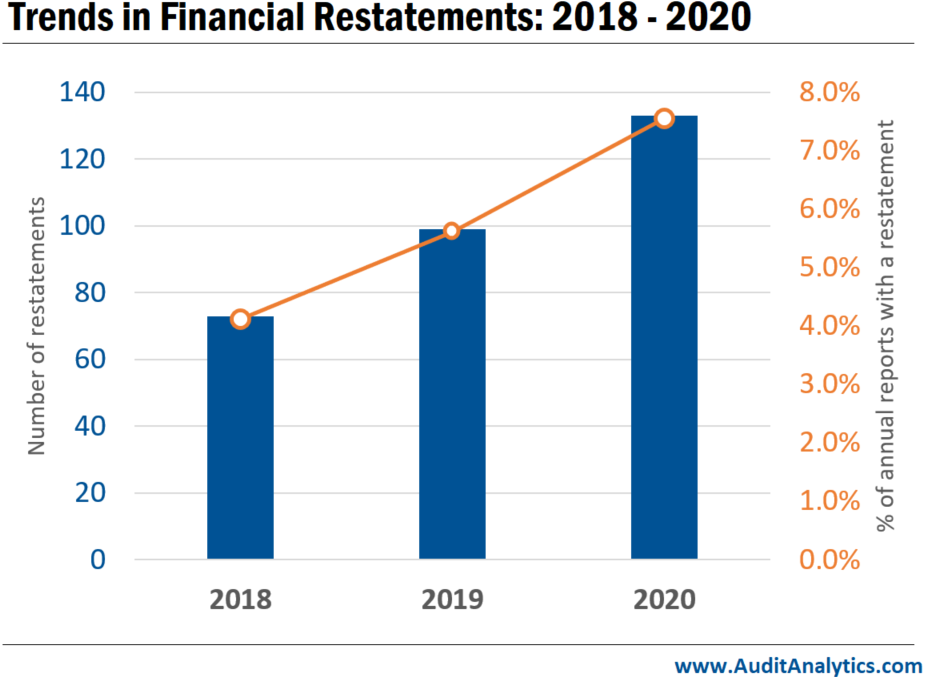

In 2018, there were 73 restatements disclosed. Then, by 2020, the number rose to 133. All in all, this represented an 82% increase in restatements over two years.

However, the 73 restatements in 2018 represented just 4.1% of companies that issued an annual report. This rose to 5.6% in 2019 and 7.6% in 2020.

Financial reporting quality and audit quality have been a main focus in the UK. A succession of reviews and proposals have been made over the past few years in response to major accounting scandals.

BHS became insolvent in 2016 following a clean audit opinion. Additionally, Carillion became insolvent in 2018 under similar circumstances. Patisserie Valerie went into administration in 2019. It was discovered that Patisserie Valeries’ financials were materially misstated.

Proposals include strengthening monitoring and reporting on internal controls, widening the scope of information assessed by the statutory auditor, and establishing a new regulator with greater authority, among other reforms.

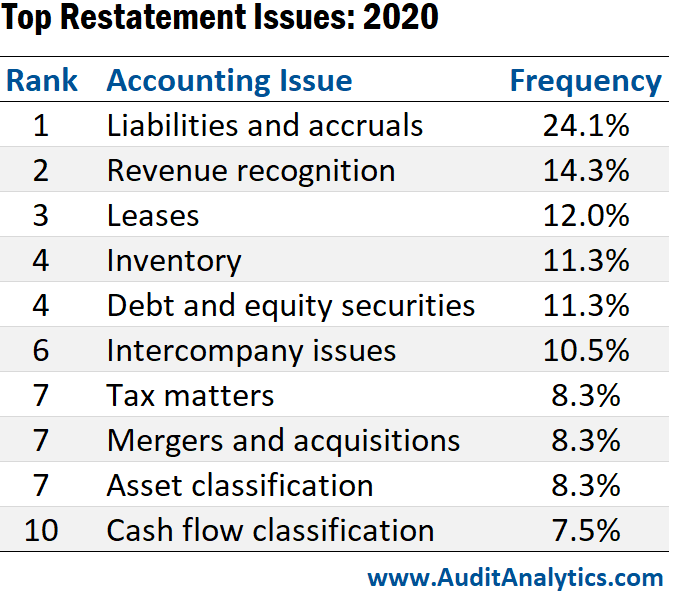

The most common accounting issue cited in 2020 was liabilities and accruals. This is in line with Canada. The second most common issue was revenue recognition, often among the most cited in the US. And leases were the third most common issue. Leases have seen a large increase in citations following the implementation of the new lease standard (IFRS 16) in 2019.

The sudden rise in UK restatements could be in response to the UK’s focus on audit and reporting quality. The circumstances are similar to the rise in US restatements following the implementation of the Sarbanes-Oxley Act of 2002. UK restatements in 2021 have outpaced 2020. So, we should expect to see a significant increase in 2021.

Interested in our content? Be sure to subscribe to receive our email notifications.