This analysis was originally posted by Audit Analytics.

This post is a part of Audit Analytics’ series on audit market concentration across select countries in Europe.

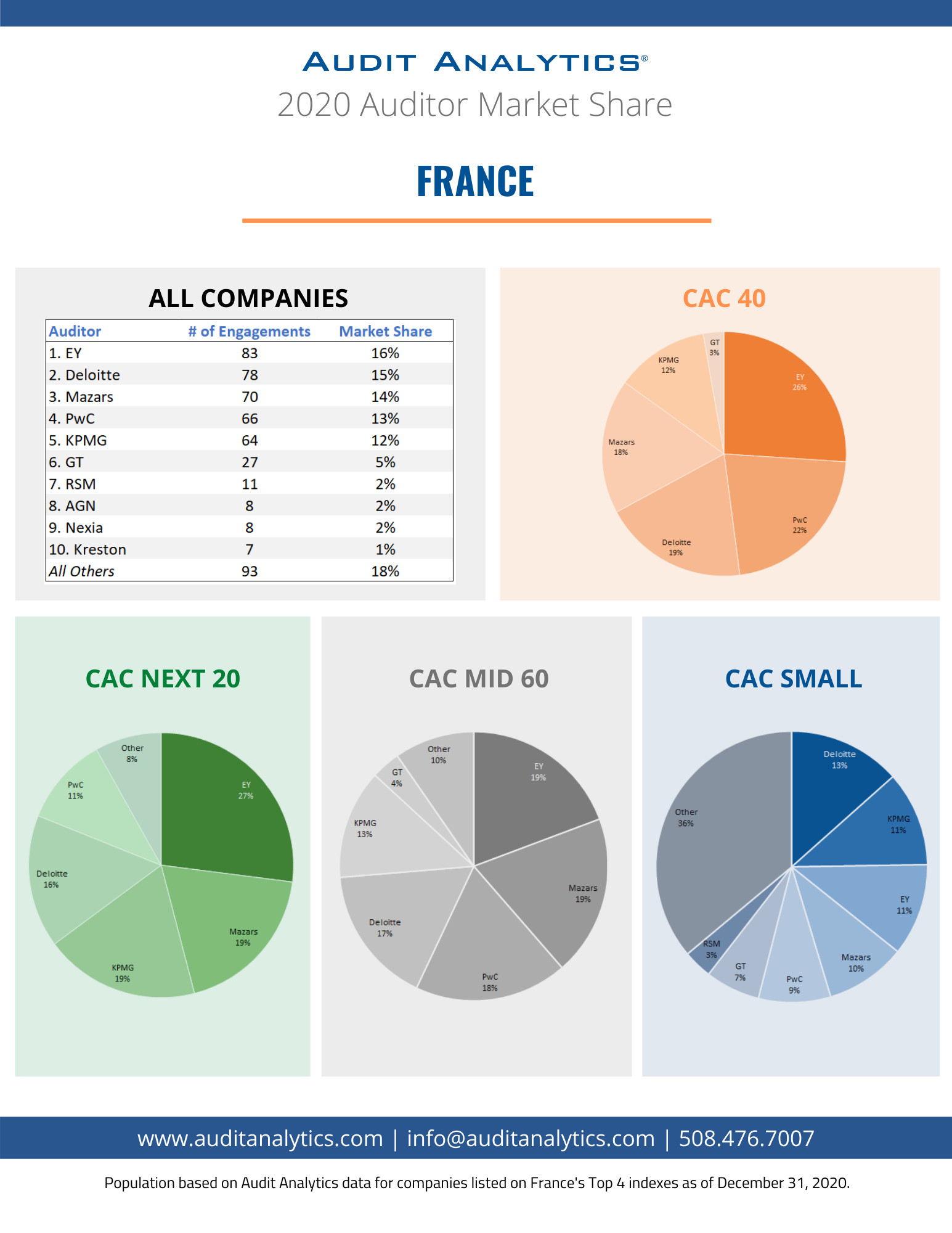

The Big Four accounting firms are collectively engaged in 57% of all French engagements, unchanged from the previous year. Deloitte led the way with 16% of all engagements, followed by EY with 15%. Mid-tier firm Mazars was third with 14% of all engagements, while PwC and KPMG round out the top five with 13% and 12%, respectively.

France is unique because of its joint audit requirement that all public interest entities (PIEs) – which include publicly listed entities – must engage at least two independent accounting firms to perform an annual audit. Many credit this requirement as creating a more diverse and competitive audit market than other countries.

CAC 40

The Big 4 continue to have a dominant role among the largest companies. Combined, the Big 4 audit 79% of the CAC 40 engagement, lead by EY with 26% of all engagements. Meanwhile, Mazars audits another 18% of CAC 40 engagements. The only other audit firm that CAC 40 companies engaged was Grant Thornton.

CAC MID 60

EY and Mazars lead with 19% of all engagements among the CAC Mid 60. In total, the Big 4 are engaged in 67% of all CAC Mid 60 engagements. Eight firms share the remaining 14% of CAC Mid 60 engagements, lead by Grant Thornton with 4%.

CAC SMALL

The CAC Small index is much more diverse, with the Big 4 plus Mazars combining for just over half (54%) of all engagements. Sixty-nine firms share the other 46% of engagements. Grant Thornton leads among smaller firms with 7% of CAC Small engagement.

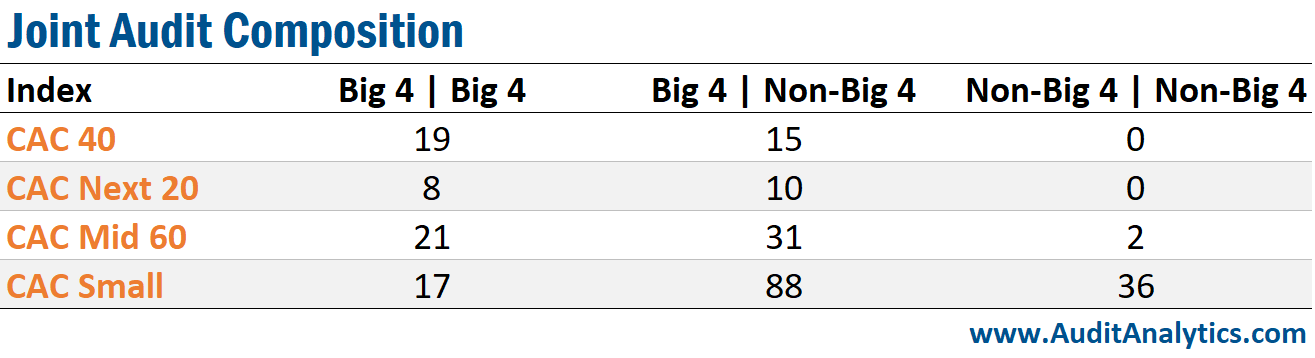

Joint Audit Market Composition

One advantage of joint audits – which is being discussed in the UK in a modified version – is the ability to engage a larger firm with greater resources to conduct a quality audit and a smaller firm with fewer resources as the joint firm. In theory, this would create a more diverse market and allow smaller firms to learn from larger firms while still ensuring quality audits.

However, in France, which is the largest market in which we have a proxy for this theory, we see limited support. Among the CAC 40, less than half of joint audit engagements include a Big 4 firm and a non-Big 4 firm. As we saw above, France’s largest mid-tier firm Mazars audits most of the non-Big 4 engagements.

Among the CAC Next 20, trends are fairly similar to the CAC 40. Nearly half of the CAC Next 20 engage two Big 4 firms. The majority of the other half that engage both a Big 4 firm and a non-Big 4 firm engage Mazars, with just two other firms engaged by CAC Next 20 companies.

Among the CAC Mid 60, nearly 60% of companies engage a Big 4 firm and non-Big 4 firm. Meanwhile, 4% engage multiple non-Big 4 firms. Most of these non-Big 4 firm engagements also include the mid-tier firm Mazars.

Among the CAC Small, nearly 90% engage at least one non-Big 4 firm. Additionally, about a quarter of CAC Small companies engage multiple non-Big 4 firms. This may be an indication that joint audits promote the use of smaller firms amongst small and mid-sized companies.

For more information about Audit Analytics or this analysis, please contact us.